Refinancing Federal Student Loans: Is It Right For You?

Table of Contents

Understanding Federal Student Loan Refinancing

What is Federal Student Loan Refinancing?

Refinancing federal student loans involves replacing your existing federal loans with a new private loan from a private lender. This process consolidates multiple loans into a single, new loan, potentially offering more favorable terms. The key difference between federal and private student loans lies in the benefits and protections offered. Federal student loans often come with income-driven repayment plans, deferment, and forbearance options, which are typically lost when refinancing into a private loan. Federal student loan types eligible for refinancing typically include Direct Subsidized Loans, Direct Unsubsidized Loans, and Direct PLUS Loans.

Benefits of Refinancing Federal Student Loans

Refinancing your federal student loans can offer several advantages:

- Lower Monthly Payments: By extending your loan term, you can significantly reduce your monthly payment amount, making your repayment more manageable. However, remember that this often means paying more interest over the life of the loan.

- Lower Interest Rates: If you have a good credit score, refinancing can secure you a lower interest rate than your original federal loans, leading to substantial savings over the loan's life. This directly impacts the total amount you pay in interest.

- Fixed Interest Rate vs. Variable: A fixed interest rate remains consistent throughout the loan term, providing predictable monthly payments. A variable interest rate fluctuates based on market conditions, creating uncertainty in your monthly budget.

- Simplified Repayment: Consolidating multiple federal loans into a single private loan streamlines your repayment process, making it easier to track and manage your debt.

- Potential for Shorter Repayment Terms: While extending the loan term lowers your monthly payments, shortening it can lead to faster debt payoff and less interest paid overall, but with higher monthly payments.

Drawbacks of Refinancing Federal Student Loans

Before you refinance, carefully consider these potential drawbacks:

- Loss of Federal Student Loan Benefits: Refinancing means losing access to federal student loan benefits such as income-driven repayment plans (IDR), deferment, and forbearance. These programs offer crucial protection during financial hardship.

- Higher Interest Rates for Borrowers with Poor Credit: Borrowers with a low credit score may not qualify for lower interest rates and may even receive higher rates than their existing federal loans. Improving your credit score before applying is highly recommended.

- Potential for Higher Overall Interest Paid: While lower monthly payments are tempting, extending your loan term often results in paying significantly more interest over the life of the loan. Carefully compare the total cost.

- Risk of Default: Failing to make your loan payments can lead to serious consequences, including damage to your credit score, wage garnishment, and even legal action.

Eligibility Requirements for Refinancing Federal Student Loans

Credit Score and Debt-to-Income Ratio

Lenders assess your creditworthiness before approving a refinance application. A higher credit score significantly improves your chances of approval and securing a favorable interest rate. Your debt-to-income ratio (DTI), which compares your monthly debt payments to your gross monthly income, also plays a vital role. A high DTI might hinder your eligibility, and you might need a co-signer.

Income and Employment Verification

Lenders require proof of stable income and employment to ensure your ability to repay the loan. They'll verify your income through pay stubs, tax returns, or bank statements. Consistent employment history is crucial for approval.

Loan Amount and Type

The total amount of your federal student loans affects your eligibility. Larger loan amounts may require a higher credit score or a co-signer. Most lenders refinance various federal loan types, but it's essential to check specific eligibility criteria with each lender.

Choosing the Right Refinancing Lender

Comparing Interest Rates and Fees

Shop around and compare interest rates and fees from multiple private lenders. Don't settle for the first offer you receive. Understand the Annual Percentage Rate (APR), which includes interest and fees, for a complete picture of the loan cost. Look out for origination fees, prepayment penalties, and other associated charges.

Reviewing Lender Reviews and Reputation

Thoroughly research potential lenders. Check online reviews and ratings from reputable sources to gauge their reputation and customer service. Look for lenders with a history of fair practices and transparent terms.

Understanding the Terms and Conditions

Before signing any loan documents, carefully read all the terms and conditions. Pay close attention to the APR, prepayment penalties (fees charged for paying off the loan early), and other crucial details. If anything is unclear, seek clarification from the lender.

Conclusion

Refinancing federal student loans can offer significant benefits, such as lower monthly payments and interest rates. However, it's crucial to carefully weigh the potential drawbacks, including the loss of federal loan benefits and the risk of higher overall interest paid. Before making a decision, thoroughly research different lenders, compare rates and fees, and carefully evaluate your financial situation. Only refinance your federal student loans if you're confident it aligns with your long-term financial goals. If you're ready to explore your refinancing options for student loan refinancing, start comparing rates from reputable lenders today. Don't hesitate to contact a financial advisor for personalized advice on refinancing federal student loans.

Featured Posts

-

Prosvjednici U Teslinom Izlozbenom Prostoru U Berlinu Prijetnja Planetu

May 17, 2025

Prosvjednici U Teslinom Izlozbenom Prostoru U Berlinu Prijetnja Planetu

May 17, 2025 -

Fortnite Latest Shop Update Sparks Player Controversy

May 17, 2025

Fortnite Latest Shop Update Sparks Player Controversy

May 17, 2025 -

Koriun Inversiones Descifrando Su Esquema Ponzi

May 17, 2025

Koriun Inversiones Descifrando Su Esquema Ponzi

May 17, 2025 -

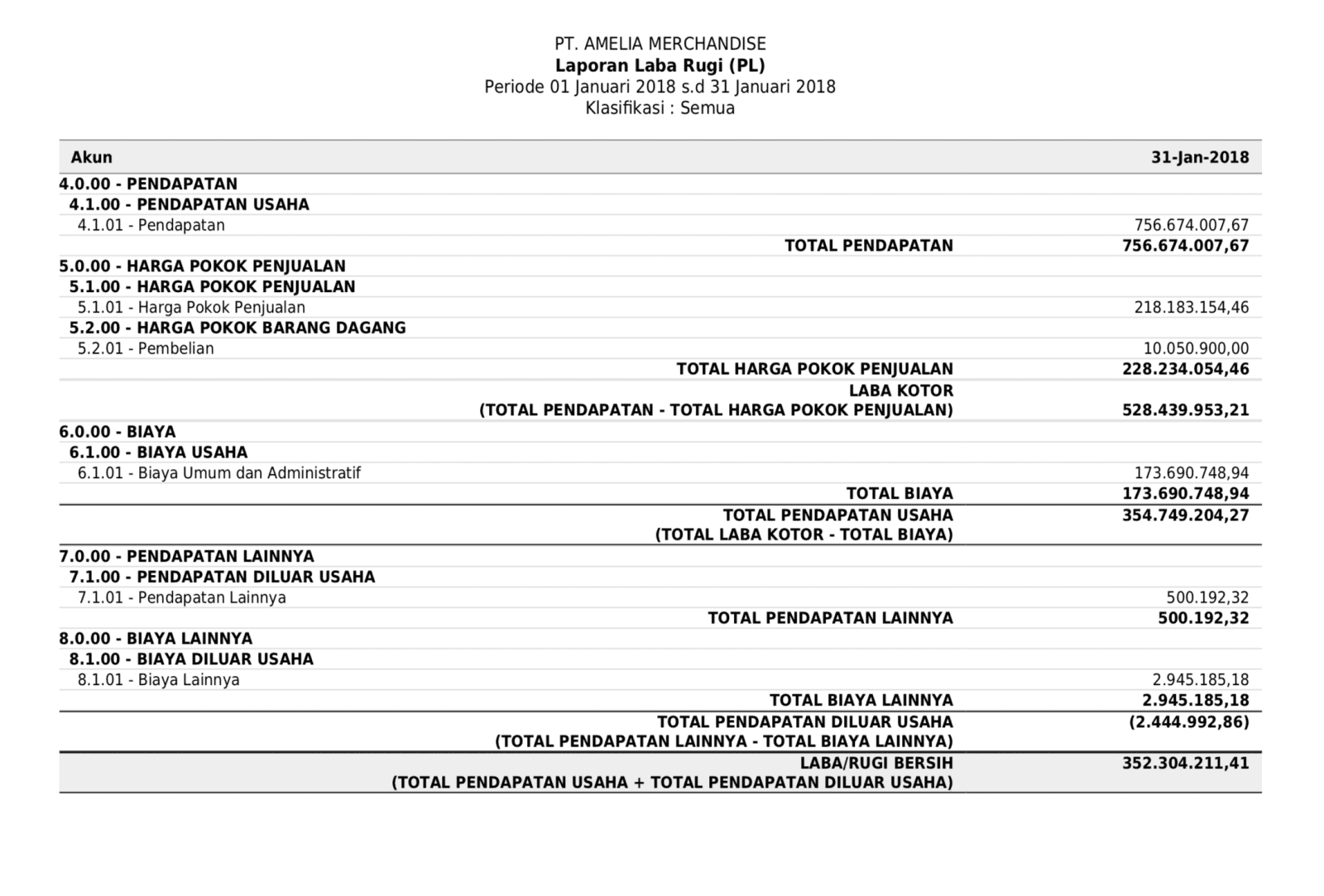

Laporan Keuangan Jenis Pentingnya Dan Manfaat Untuk Bisnis Anda

May 17, 2025

Laporan Keuangan Jenis Pentingnya Dan Manfaat Untuk Bisnis Anda

May 17, 2025 -

Pistons Vs Knicks Key Factors Determining Success This Season

May 17, 2025

Pistons Vs Knicks Key Factors Determining Success This Season

May 17, 2025

Latest Posts

-

Analyzing The Knicks Challenges Beyond Brunsons Injury

May 17, 2025

Analyzing The Knicks Challenges Beyond Brunsons Injury

May 17, 2025 -

Knicks Post Brunson Performance A Concerning Trend

May 17, 2025

Knicks Post Brunson Performance A Concerning Trend

May 17, 2025 -

Ankle Injury Forces Jalen Brunson Out Of Knicks Lakers Game

May 17, 2025

Ankle Injury Forces Jalen Brunson Out Of Knicks Lakers Game

May 17, 2025 -

Brunsons Overtime Ankle Injury Costs Knicks Lakers Game

May 17, 2025

Brunsons Overtime Ankle Injury Costs Knicks Lakers Game

May 17, 2025 -

Knicks Depth A Silver Lining In Jalen Brunsons Injury

May 17, 2025

Knicks Depth A Silver Lining In Jalen Brunsons Injury

May 17, 2025