Successfully Buying A Home Despite Student Loan Debt

Table of Contents

Assessing Your Financial Situation & Credit Score

Before you even start browsing properties, understanding your financial health is crucial. This involves analyzing your debt-to-income ratio (DTI) and improving your credit score. Both are key factors lenders consider when evaluating your mortgage application.

Understanding Your Debt-to-Income Ratio (DTI)

Your debt-to-income ratio is a crucial metric that lenders use to assess your ability to repay a mortgage. It represents the percentage of your gross monthly income that goes towards debt payments. A lower DTI generally increases your chances of mortgage approval and securing a favorable interest rate. Student loan payments significantly impact your DTI, so it's vital to understand how they factor into the equation.

Calculating your DTI involves adding up all your monthly debt payments (including student loans, credit cards, car payments, etc.) and dividing that total by your gross monthly income. For example:

- Monthly Debt Payments: $1,500 (including $500 in student loan payments)

- Gross Monthly Income: $5,000

- DTI: ($1,500 / $5,000) x 100% = 30%

A DTI of 30% is generally considered acceptable, but lenders may prefer a lower ratio. The impact of your student loan payments on your DTI is significant. Strategies to lower your DTI include:

- Check your credit report regularly for errors. Inaccurate information can negatively affect your credit score and DTI.

- Focus on paying down high-interest debt. This will free up more of your income for mortgage payments.

- Consider debt consolidation options to lower monthly payments. This can simplify your finances and potentially lower your DTI.

Improving Your Credit Score

A good credit score is essential for securing a mortgage with favorable terms. Lenders use your credit score to assess your creditworthiness and determine the interest rate they'll offer. Your student loan payment history significantly impacts your credit score. Consistent on-time payments demonstrate financial responsibility, while missed payments can severely damage your credit.

Here are some practical steps to improve your credit score:

- Pay all bills on time. This is the single most important factor in your credit score.

- Keep credit utilization low. Try to keep your credit card balances below 30% of your credit limit.

- Monitor your credit reports regularly. Check for any errors and dispute inaccurate information promptly.

- Dispute any inaccurate information. Errors on your credit report can hurt your score.

Exploring Mortgage Options & Down Payment Strategies

With student loan debt, choosing the right mortgage and saving for a down payment requires careful planning. Several mortgage options cater to borrowers with existing debt.

Types of Mortgages for Buyers with Student Loan Debt

Several mortgage types can help you navigate home buying with student loan debt:

- FHA Loans: These government-insured loans often require lower down payments (as low as 3.5%), making them attractive to buyers with limited savings. However, they typically come with mortgage insurance premiums.

- Conventional Loans: These loans aren't backed by the government, so they may require higher credit scores and larger down payments (often 20%). However, they can sometimes offer better interest rates than FHA loans.

- USDA Loans: These loans are specifically designed for rural properties and often require no down payment. Eligibility is based on location and income.

Saving for a Down Payment

Saving for a down payment while managing student loan payments can seem daunting. However, with a realistic plan and commitment, it is achievable.

- Create a realistic budget. Track your income and expenses to identify areas where you can cut back.

- Automate savings. Set up automatic transfers from your checking to your savings account each month.

- Explore down payment assistance programs. Many state and local governments offer programs to help first-time homebuyers.

- Consider gift funds from family. If possible, talk to family members about potentially contributing to your down payment.

Negotiating with Lenders & Communicating Your Financial Situation

Open and honest communication with lenders is key to successfully securing a mortgage. Understanding the pre-approval process and effectively presenting your financial situation, including your student loan debt, are essential steps.

Preparing for Pre-Approval

Pre-approval is a crucial step in the home-buying process. It shows sellers that you're a serious buyer and strengthens your offer. To prepare for pre-approval, gather the following documents:

- Pay stubs

- Tax returns

- Bank statements

- Student loan repayment information

Shop around for the best mortgage rates and be prepared to answer lender questions thoroughly and honestly.

Effectively Communicating with Lenders About Student Loan Debt

Don't shy away from discussing your student loan debt; instead, frame it positively.

- Be transparent about your student loans. Don't try to hide them.

- Highlight your consistent payment history. Show that you're a responsible borrower.

- Emphasize your overall financial stability. Showcase your ability to manage your finances effectively, despite your student loans.

Conclusion

Successfully buying a home while managing student loan debt requires careful planning and a strategic approach. By assessing your financial situation, improving your credit score, exploring diverse mortgage options, and effectively communicating with lenders, you can significantly increase your chances of homeownership. Remember to prioritize responsible debt management, diligently save for a down payment, and utilize available resources. Don't let student loan debt derail your dream of homeownership – take control of your finances, and start your journey toward successfully buying your dream home today! Start planning your home purchase despite your student loan debt now!

Featured Posts

-

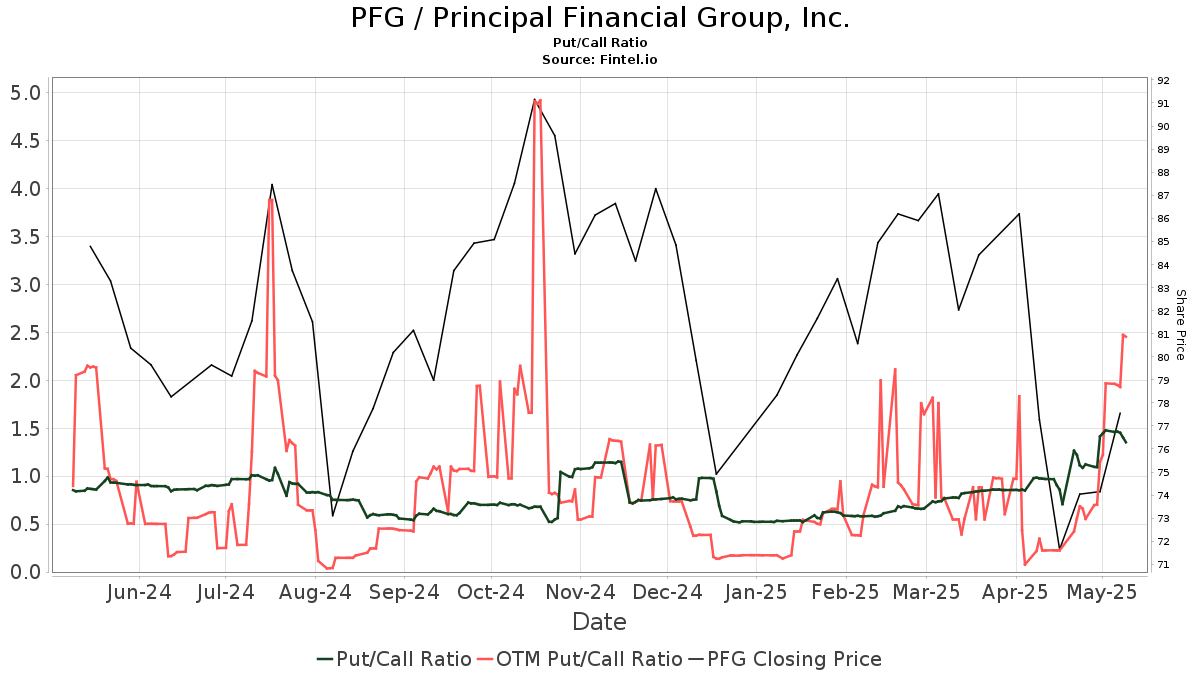

Analyzing Principal Financial Group Pfg What 13 Analysts Say

May 17, 2025

Analyzing Principal Financial Group Pfg What 13 Analysts Say

May 17, 2025 -

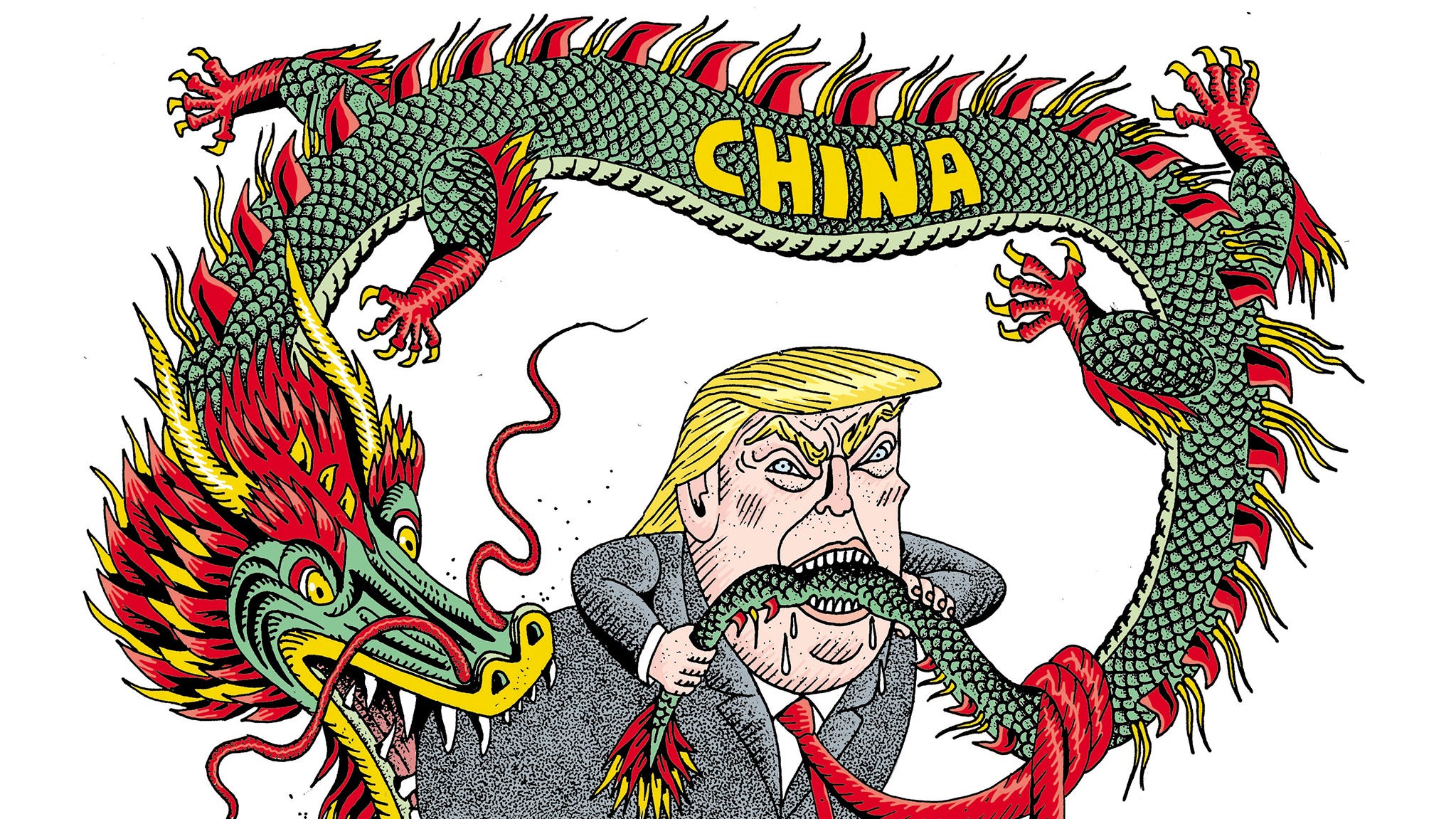

Trumps China Tariffs A 30 Hold Through 2025 And Beyond

May 17, 2025

Trumps China Tariffs A 30 Hold Through 2025 And Beyond

May 17, 2025 -

Ncaa Game Win Angel Reese Honors Mom With Emotional Message Of Support

May 17, 2025

Ncaa Game Win Angel Reese Honors Mom With Emotional Message Of Support

May 17, 2025 -

Technical Glitch Forces Blue Origin To Postpone Rocket Launch

May 17, 2025

Technical Glitch Forces Blue Origin To Postpone Rocket Launch

May 17, 2025 -

Knicks Fans Petition Replacing Lady Liberty With Jalen Brunson

May 17, 2025

Knicks Fans Petition Replacing Lady Liberty With Jalen Brunson

May 17, 2025

Latest Posts

-

Ex Vasco Brilha Nos Emirados E Sonha Com A Copa Do Mundo De 2026

May 17, 2025

Ex Vasco Brilha Nos Emirados E Sonha Com A Copa Do Mundo De 2026

May 17, 2025 -

Remembering Jean Marsh A Career Celebrating Upstairs Downstairs And Beyond

May 17, 2025

Remembering Jean Marsh A Career Celebrating Upstairs Downstairs And Beyond

May 17, 2025 -

Favelas Als Investitionschance Das Engagement Der Vereinigten Arabischen Emirate In Brasilien

May 17, 2025

Favelas Als Investitionschance Das Engagement Der Vereinigten Arabischen Emirate In Brasilien

May 17, 2025 -

Birlesik Arap Emirlikleri Ve Tuerkiye Erdogan In Telefon Goeruesmesinin Ardindan

May 17, 2025

Birlesik Arap Emirlikleri Ve Tuerkiye Erdogan In Telefon Goeruesmesinin Ardindan

May 17, 2025 -

Ex Vasco Camisa 10 Nos Emirados Arabes Mira Copa 2026

May 17, 2025

Ex Vasco Camisa 10 Nos Emirados Arabes Mira Copa 2026

May 17, 2025