Homeownership With Student Loans: Tips And Strategies For Success

Table of Contents

Assessing Your Financial Situation

Before you even start browsing open houses, a thorough assessment of your financial situation is crucial. This involves understanding your debt, creating a realistic budget, and improving your credit score – all key factors in securing a mortgage while managing student loan payments.

Understanding Your Debt

Analyze your student loan debt meticulously. This includes identifying the interest rates, repayment plans, and the total amount owed for each loan.

- Different Repayment Plans: Explore various options like Standard Repayment, Graduated Repayment, Extended Repayment, and Income-Driven Repayment (IDR) plans. Each has different implications for your monthly payments and overall repayment time.

- Credit Report Check: Regularly check your credit report for any errors that could impact your credit score and mortgage approval. Services like AnnualCreditReport.com allow you to access your reports for free.

- Interest Capitalization: Understand how interest capitalization works. This is when unpaid interest is added to your principal loan balance, increasing the total amount you owe.

High debt-to-income (DTI) ratios, which compare your monthly debt payments to your gross monthly income, can significantly affect your mortgage pre-approval. Lenders typically prefer lower DTI ratios, so understanding your DTI is essential.

Budgeting for Homeownership

Creating a realistic budget that incorporates all expenses is paramount. This isn't just about your current spending; it's about projecting your expenses as a homeowner.

- Budgeting Apps: Utilize budgeting apps like Mint, YNAB (You Need A Budget), or Personal Capital to track your income and expenses effectively.

- Meticulous Tracking: Track every expense, from groceries to entertainment, to understand where your money is going.

- Reduce Spending: Identify areas where you can cut back on expenses to free up funds for your mortgage and student loan payments.

Unexpected expenses are inevitable. Having a robust emergency fund – ideally 3-6 months of living expenses – will cushion the blow and prevent you from falling behind on your payments.

Improving Your Credit Score

A higher credit score translates to better mortgage rates and terms. Improving your score before applying for a mortgage is a smart move.

- On-Time Payments: Always pay your bills on time. This is the single most important factor influencing your credit score.

- Credit Utilization: Keep your credit utilization low (ideally below 30%). This refers to the amount of credit you're using compared to your total available credit.

- Dispute Errors: Check your credit report regularly and dispute any inaccuracies you find.

A higher credit score can save you thousands of dollars in interest over the life of your mortgage.

Exploring Mortgage Options

Understanding the various mortgage options available is crucial for finding the best fit for your financial situation.

Types of Mortgages

Several mortgage types cater to different borrowers, including those with student loan debt.

- FHA Loans: These loans require lower down payments and have more lenient credit score requirements, making them potentially accessible to borrowers with student loans.

- VA Loans: Offered to eligible veterans and military personnel, VA loans often require no down payment and have competitive interest rates.

- Conventional Loans: These loans are offered by private lenders and generally require higher credit scores and down payments.

Each mortgage type comes with its own set of advantages, disadvantages, down payment requirements, and potential closing costs. Researching these aspects thoroughly is vital.

Finding the Right Lender

Shopping around for the best mortgage rates and terms is essential. Don't settle for the first offer you receive.

- Compare Rates and Fees: Compare interest rates, fees, and closing costs from multiple lenders.

- Lender Reviews: Check online reviews and ratings of different lenders to gauge their reputation and customer service.

- Pre-qualification vs. Pre-approval: Understand the difference. Pre-qualification provides a general estimate of how much you can borrow, while pre-approval involves a more thorough review of your finances and significantly strengthens your offer when purchasing a home.

Strategies for Managing Student Loans and Mortgage Payments

Juggling student loans and a mortgage requires a well-defined strategy.

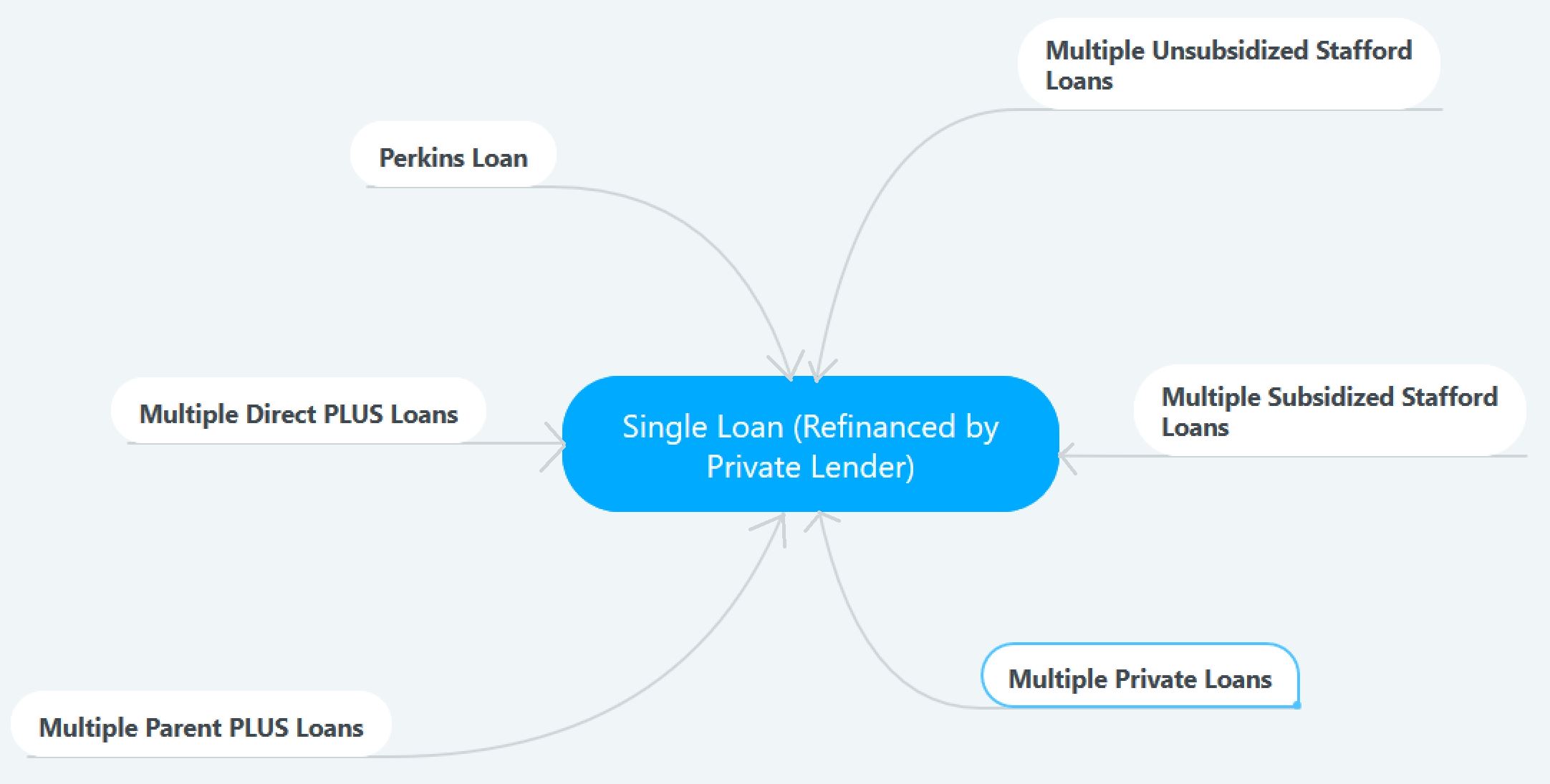

Refinancing Student Loans

Refinancing your student loans might lower your interest rates, resulting in lower monthly payments.

- Pros and Cons: Carefully weigh the pros and cons. While lower rates are attractive, refinancing could impact your eligibility for income-driven repayment plans.

- Eligibility Requirements: Check your eligibility based on your credit score and income.

- Impact on Credit Score: The application process might temporarily impact your credit score.

Income-Driven Repayment Plans (IDRP)

IDRP plans base your monthly student loan payments on your income and family size.

- Different Types: Explore plans like PAYE, REPAYE, IBR, and ICR to find the one best suited to your circumstances.

- Eligibility Criteria: Understand the eligibility requirements for each plan.

- Long-Term Implications: Be aware that these plans often extend your repayment period, leading to higher total interest paid over the life of the loan.

Prioritizing Payments

Develop a system to prioritize essential expenses, including your mortgage and student loan payments.

- Budgeting Techniques: Use budgeting techniques like the 50/30/20 rule or zero-based budgeting to allocate funds effectively.

- Automate Payments: Set up automatic payments to avoid late fees and ensure consistent payments.

- Consequences of Missed Payments: Missed payments on both your mortgage and student loans can have severe consequences, including damaging your credit score and potentially leading to foreclosure or loan default.

Conclusion

Achieving homeownership while managing student loan debt requires careful planning and strategic execution. By assessing your financial situation, exploring different mortgage options, and employing effective strategies for managing your student loans, you can significantly increase your chances of successfully navigating this journey. Remember, consistent budgeting, smart financial decisions, and seeking professional financial advice can all contribute to your success in achieving your dream of homeownership with student loans. Start planning today and take control of your financial future! Start your homeownership journey today, even with student loans!

Featured Posts

-

North Dakotas Leading Philanthropist Receives Msum Honorary Degree

May 17, 2025

North Dakotas Leading Philanthropist Receives Msum Honorary Degree

May 17, 2025 -

Fortnites Most Exclusive Skins Will They Ever Come Back

May 17, 2025

Fortnites Most Exclusive Skins Will They Ever Come Back

May 17, 2025 -

Is Refinancing Federal Student Loans Worth It A Practical Analysis

May 17, 2025

Is Refinancing Federal Student Loans Worth It A Practical Analysis

May 17, 2025 -

Koriun Descongelacion De Cuentas E Informacion Para Inversionistas

May 17, 2025

Koriun Descongelacion De Cuentas E Informacion Para Inversionistas

May 17, 2025 -

Fortnite Item Shop Enhanced A New Feature For Players

May 17, 2025

Fortnite Item Shop Enhanced A New Feature For Players

May 17, 2025

Latest Posts

-

The Luka Doncic Trade And Jalen Brunsons Free Agency Which Hit The Dallas Mavericks Harder

May 17, 2025

The Luka Doncic Trade And Jalen Brunsons Free Agency Which Hit The Dallas Mavericks Harder

May 17, 2025 -

Mavs Setbacks A Side By Side Look At The Brunson Departure And The Doncic Trade Buzz

May 17, 2025

Mavs Setbacks A Side By Side Look At The Brunson Departure And The Doncic Trade Buzz

May 17, 2025 -

Comparing Impacts Jalen Brunsons Free Agency And The Luka Doncic Trade Speculation For The Mavericks

May 17, 2025

Comparing Impacts Jalen Brunsons Free Agency And The Luka Doncic Trade Speculation For The Mavericks

May 17, 2025 -

The Fifteenth Doctors New Companion Facing Killer Cartoons In Doctor Who Season 2 Trailer

May 17, 2025

The Fifteenth Doctors New Companion Facing Killer Cartoons In Doctor Who Season 2 Trailer

May 17, 2025 -

Knicks Narrow Escape An Overtime Loss And The Potential For Disaster

May 17, 2025

Knicks Narrow Escape An Overtime Loss And The Potential For Disaster

May 17, 2025